Vietnam Legislation v3.0.1 for Sage X3: Bad Debt Management in Compliance with Circular 99/2025

Introduction

Bad debt is an inevitable reality for businesses that extend credit to customers. When a customer fails to pay their outstanding balance and the debt becomes uncollectible, companies must recognize this as a bad debt expense. Proper management of bad debts is essential for accurate financial reporting and tax compliance.

In Vietnam, Circular 99/2025/TT-BTC provides specific guidelines on provisioning and writing off doubtful debts. This article will explore how the Bad Debt Management functionality of Sage X3 can be configured and updated in the Vietnam Legislation package v3.0.1 to comply with Vietnamese legal regulations.

Understanding Bad Debt in Business Context

Bad debt represents an expense incurred when credit previously extended to a customer is deemed uncollectible. This is a contingency that all credit-granting companies must account for, as there is always inherent risk in extending credit.

Two Main Estimation Methods

There are two primary approaches to estimating allowances for bad debts:

- Percentage Sales Method – Estimates bad debt as a percentage of credit sales

- Accounts Receivable Aging Method – Categorizes receivables by age and applies increasing provision rates to older debts

Sage X3 Bad Debt Management Overview

Sage X3 provides a flexible bad debt process supporting three transaction types:

| Type | Description | Reversible |

|---|---|---|

| Doubtful Receivables | Initial provision for potentially uncollectible debts | Yes |

| Impairments | Recognition of value reduction in receivables | Yes |

| Write-off | Final removal of uncollectible debt from books | No |

Key Features

- Flexible percentage configuration for default calculations

- Reversal capability for doubtful receivables and impairments

- Customizable automatic journals

- Full traceability with drill-down to original transactions

Vietnam Legislation: Circular 99/2025

Provision Rates for Doubtful Accounts

Regulations stipulate that bad debt provisions are determined based on the number of overdue days of accounts receivable (Accounts Receivable Aging Method).

| Days Overdue | Rate | Description |

|---|---|---|

| 180 – 365 days | 30% | 6 months to less than 1 year |

| 366 – 730 days | 50% | 1 year to less than 2 years |

| 731 – 1,095 days | 70% | 2 years to less than 3 years |

| > 1,096 days | 100% | 3 years or more |

Accounting Entries

Bad Debt Provision:

- Debit: Expense Account

- Credit: Bad Debt Provision Account (229)

Write-off bad debts:

- Debit: Bad Debt Provision Account (229)

- Credit: Account Receivable (131)

Configuration Highlights

This functionality has been specifically enhanced in the Vietnam Legislation V3.0.1 update to ensure precise compliance. Key configuration highlights include:

Automatic Journals for Vietnam

| Code | Description | Standard Reference |

|---|---|---|

| YBDR | Bad Debt Provision | BDDBR |

| YBDIM | Impairments | BDIMP |

| YBDWO | Write-off | BDWO |

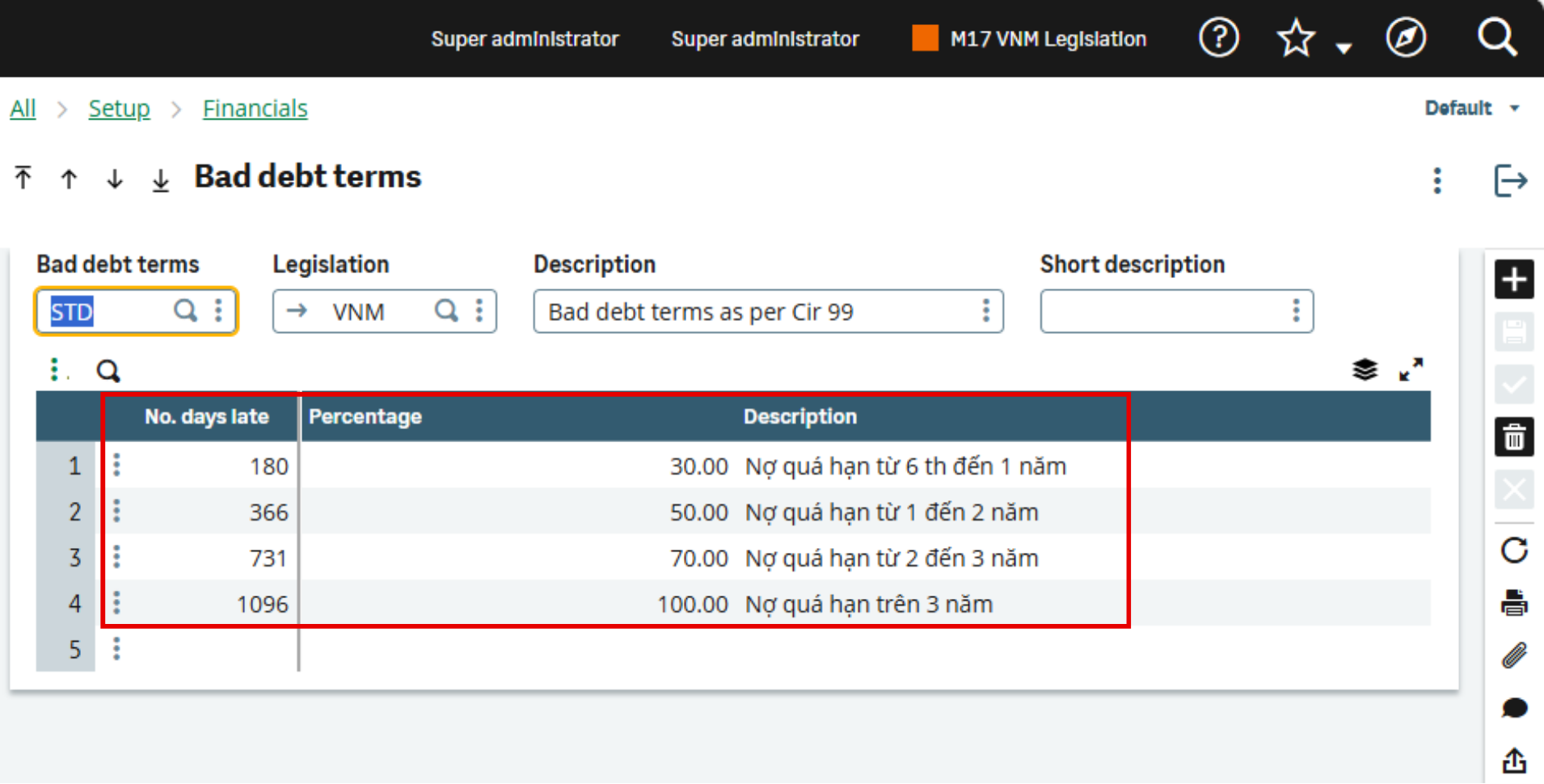

Bad Debt Terms (per Circular 99/2025)

| Days Late | Percentage | Description |

|---|---|---|

| 180 | 30% | 6 months to less than 1 year |

| 366 | 50% | 1 year to less than 2 years |

| 731 | 70% | 2 years to less than 3 years |

| 1096 | 100% | 3 years or more |

Using Bad Debt Management

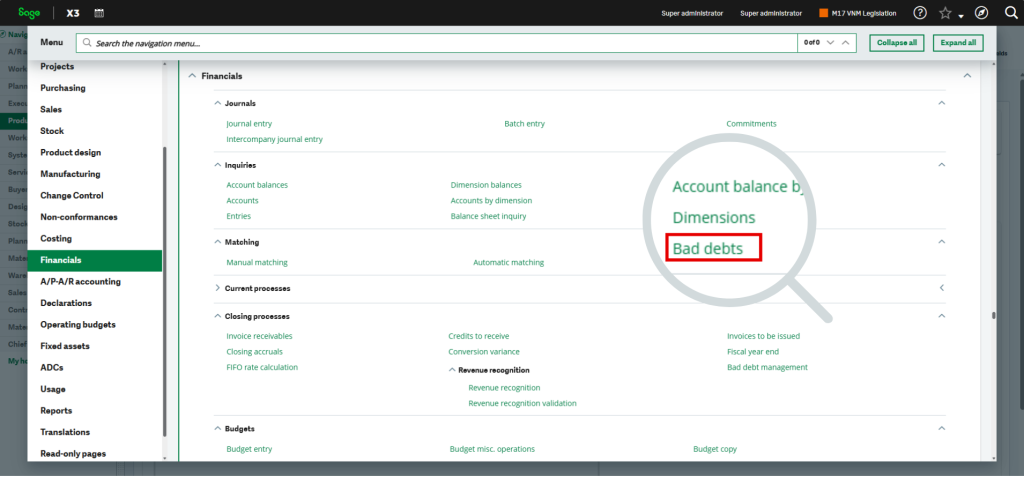

Accessing the Function

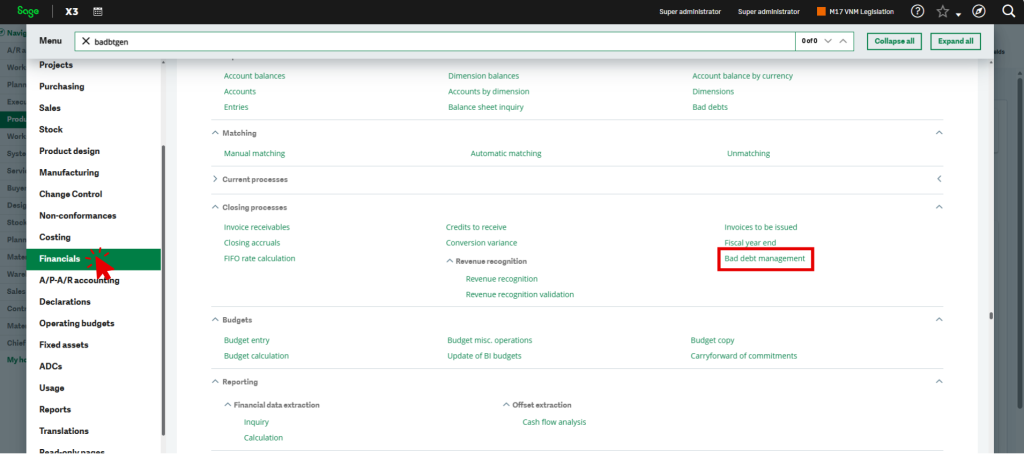

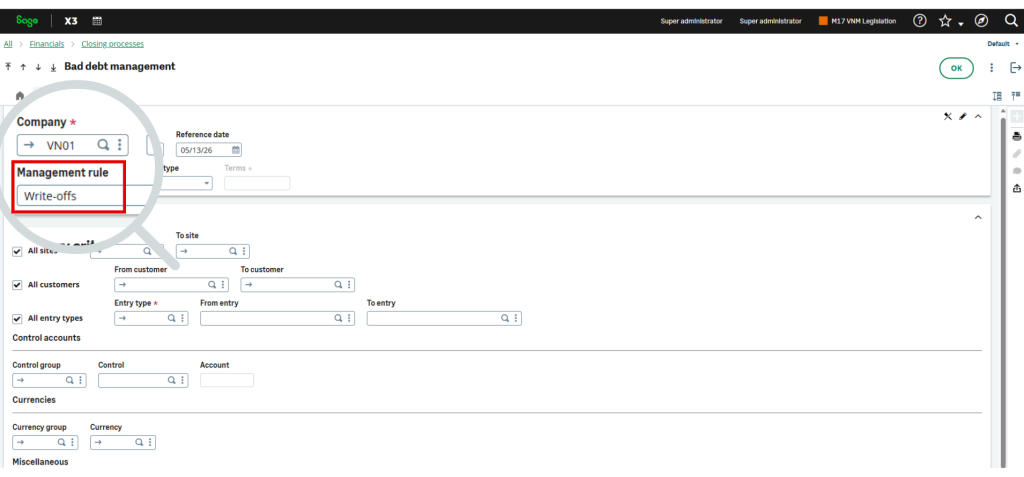

Navigate to: Financials > Closing Processes > Bad Debt Management (BADBTGEN)

Key Selection Criteria

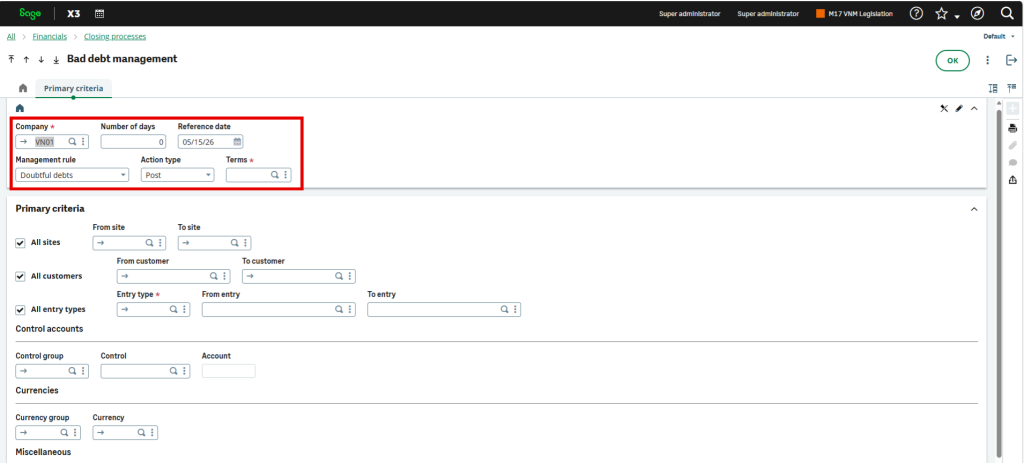

When processing bad debts, users must specify:

- Company (mandatory)

- Number of Days – Filter for documents older than reference date minus this value

- Reference Date – Date used for filtering (accounting date or due date based on parameter BDTDR)

- Management Rule – Doubtful debts, Impairments, Write-offs, or All methods

- Action Type – Post (create new) or Reverse (revert previously created)

- Terms – Pre-configured bad debt terms for percentage calculations

Post Process

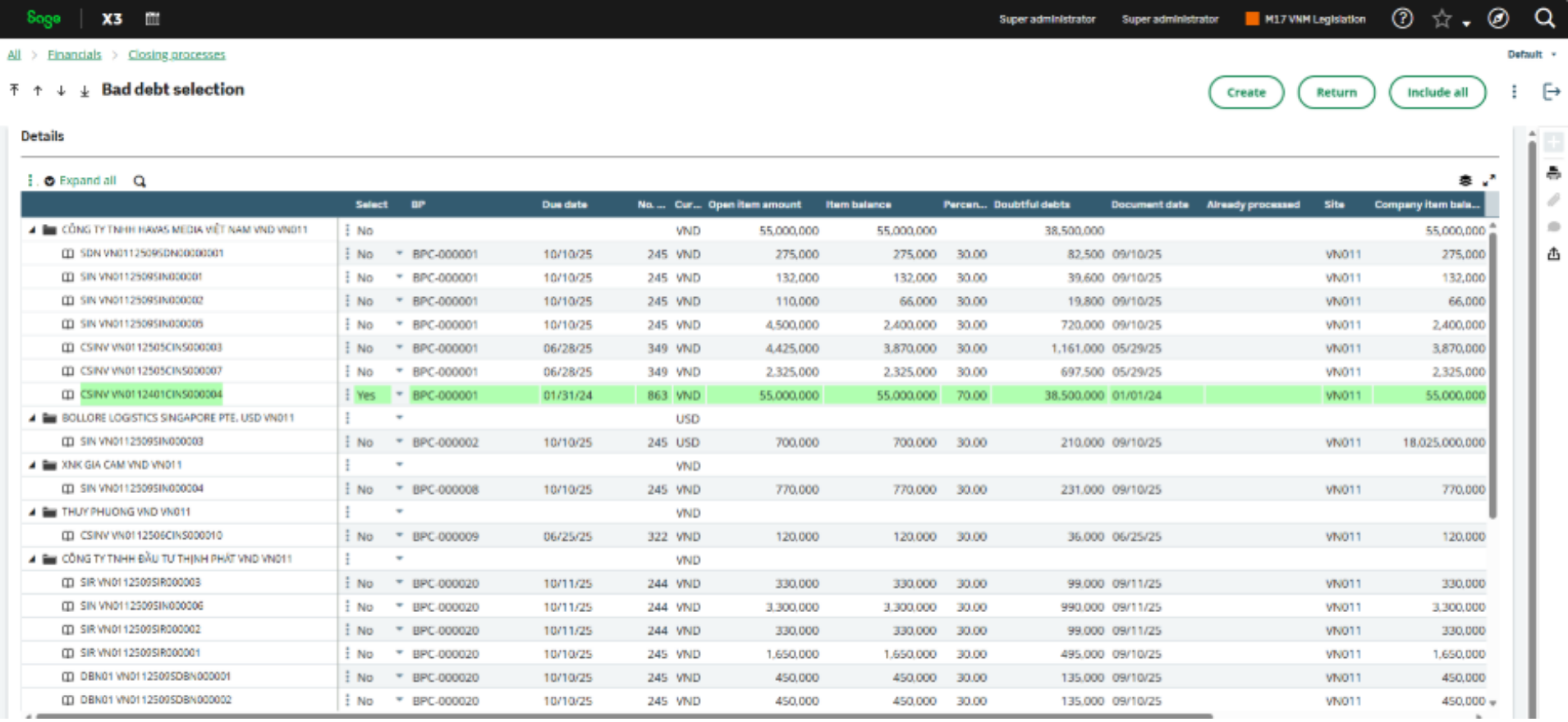

- Define selection criteria and click “OK”

- Review the grid displaying filtered open items by BP

- Select items to process (rows turn green when selected)

- Adjust percentages or amounts if needed

- Click “Create” and specify the accounting date

- Journal entries are automatically generated and logged

Reverse Process

The reversal process is available only for Doubtful Receivables and Impairments. Write-offs cannot be reversed.

- Select “Reverse” as the Action Type

- Choose documents to reverse from the filtered list

- Modify reversal amounts if partial reversal is needed

- Click “Create” to generate reversal entries

- The system automatically performs matching if required

Write-off Process

Important: According to Circular 99/2025, write-offs must first utilize the allowance for doubtful debts to offset the receivable.

Conditions for Legal Write-off:

- Documentation of debtor insolvency (bankruptcy, liquidation, death, or disappearance)

- Debt overdue for 3 years or more (100% provision rate)

- Exhaustion of collection remedies through legal means

Bad Debt Inquiry

Navigate to: Financials > Inquiries > Bad Debts (CONSBDT)

This inquiry function allows users to review all bad debt documents with filters for:

- Company and Site

- Date range

- Business Partner

- Management rule type

Results display includes original open items, bad debt documents, amounts, and accounting dates. Reversal amounts are highlighted in red for easy identification.

Key Benefits

Bad‑debt provisioning and write‑offs aren’t just about compliance; they’re about running a tighter business. With Sage X3 and Vietnam Legislation package of Ekino, Circular 99/2025 becomes a built‑in rulebook, you calculate, post, reverse where appropriate, write off when necessary, and report with confidence

- Regulatory Compliance – Aligned with Circular 99/2025

- Automation – Reduces manual entry errors

- Traceability – Complete audit trail

- Multi-currency Support – VND and other currencies

Whether you need a quick readiness check, a Vietnam-ready template for your folder, or implementation assistance to help limit bad debt risk, the ekino Vietnam team can help you get there fast and stay audit-proof. Contact us at contact@ekino.vn